Contents:

None of the 3 types of free cash flow consider depreciation as a cash-reducing item because depreciation is non-cash. We can therefore calculate FCFF by starting with earning before interest and tax . Since we want to eliminate the impact of interest on tax payment, we will simply calculate the taxes due on this amount. We call the result of this calculation NOPAT — net operating profit after tax. Free Cash Flow is important because it’s remarkably easy to calculate and can be quickly used as the basis for a valuation scenario. Operating profit is the total earnings from a company’s core business operations, excluding deductions of interest and tax.

- Whenever we are confronted with IRR analysis, it is important to understand what kind of IRR is calculated, IRR levered or IRR unlevered.

- IRR Unlevereduses the unlevered freecash flowsand is subject to the operating risks of the company.

- In the case where the company has negative unlevered free cash flow, it might not necessarily be an indication that the company is not doing well.

- IRR and levered IRR are calculated the same way, as we will see below.

- For instance, they are categorized as operating, investing, and financing expenses that can be analyzed by users of the financial statement to assess which particular head took up most of the cash of the company.

First, levered IRR is a return metric that should be calculated as part of the pre-investment due diligence process to help drive investment decisions about whether or not to purchase a specific property. In the levered scenario, the addition of debt boosts the IRR to 25.18%, which demonstrates why debt can be so beneficial in a real estate transaction – it can drive higher returns. Just as each business is unique, so is the reasoning behind why a company wants to showcase free cash flows as part of its balance sheet. Levered free cash flow uses a change in net working capital as part of the equation.

It ensures calculating Equity Value instead of Enterprise Value. While calculating valuation multiples, we often use either Enterprise Value or Equity Value in the numerator with some cash flow metric in the denominator. While we almost always use both Enterprise Value and Equity Value multiples, it is extremely important to understand when to use which. If the denominator includes interest expense, Equity Value is used, and if it does not include interest expense, Enterprise Value is used.

Unlevered IRR vs Levered IRR: What’s the Difference?

To better understand these differences, let’s walk through an example starting with the unlevered returns. It’s typical to assess the value of a real estate portfolio on a quarterly basis to ensure the cap rate is still accurate. Navigate through the world of real estate investing with Fintor learning guides.

Now that we’ve explored how to think about levered and unlevered free cash flow, let’s look at different formulas for calculating them and answer common questions. Unlevered free cash flow is the cash flow a business has, excluding interest payments. Essentially, this number represents a company’s financial status if they were to have no debts. Unlevered free cash flow is also referred to as UFCF, free cash flow to the firm, and FFCF. Before looking into the difference between FCFF vs FCFE, it is important to understand what exactly is Free Cash Flow . Free Cash Flow is the amount of cash flow a firm generates after taking into account non-cash expenses, changes in operating assets and liabilities, and capital expenditures.

eFinancial Models

Net working capital is the difference between assets and liabilities. Depending on which type of free cash flow metric a company uses, there are different financial obligations to satisfy before stating the final amount. Cash Flows are considered to be one of the most important financial metrics within the company.

SL Green Realty Corp. (SLG) Q3 2022 Earnings Call Transcript – Seeking Alpha

SL Green Realty Corp. (SLG) Q3 2022 Earnings Call Transcript.

Posted: Thu, 20 Oct 2022 07:00:00 GMT [source]

Instead, real estate investors should create a proforma projection of cash flows for a defined holding period and use an IRR function in a spreadsheet to calculate it. However, along with unlevered cash flow, stakeholders also need to include pieces of information that are more relevant to the financial statements of the company. In other words, they should ensure that they also take into consideration other relevant things, like the total debt that has been taken on by the company, because that needs to be duly honored too. The formula that is used in order to calculate unlevered cash flow does not take into account debt or any payments that have to be made in order to settle the debts.

What is a Levered IRR?

The overall https://1investing.in/ rate in this case is equal to the mortgage yield rate. In other words, as we add more debt to this property under these loan terms, the equity yield will not change. The overall yield rateis the internal rate of return on all property cash flows, including the proceeds from sale, at the end of the investment. Unlevered IRR or unleveraged IRR is the internal rate of return of a string of cash flows without financing.

Therefore, by this definition, irr levered vs unlevered cash flows simply imply that they do not include debt-related components within the company. Hence, unlevered cash flow is merely representative of the cash that the firm has for all of its stakeholders, which also include the debt holders of the company. Further description and analysis of both levered and unlevered cash flow are given below.

When using a levered free cash flow formula, the company is obligated to settle on expenses and amounts owed to debt holders prior to calculating a final total. With the above definitions in mind, unlevered free cash flow does not include expenses, while levered free cash flow factors them in. If you remember one rule of thumb regarding cash flows, it should be this.

Negative leverageoccurs when the overall yield rate is less than the mortgage yield rate. When this happens, the equity yield rate will be less than the overall yield rate. For a multi-year analysis of leverage, the overall yield rate is compared to the mortgage yield rate. A capitalization rate is just a fraction used to express the relationship between income in a single year and the value of an asset. On an unlevered basis, returns are lower because the upfront investment is higher. If you wanted to double your money every 5 years you would need to generate an annual rate of return of 14.4%.

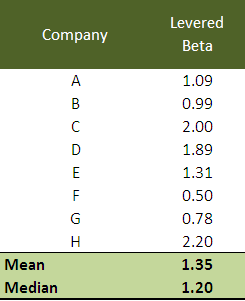

The equity capitalization rateis the cash flow before tax in a single year divided by the equity investment. This is also known as the cash on cash return or equity dividend rate. The unlevered cost of capital represents the cost of a company financing the project itself without incurring debt. It provides an implied rate of return, which helps investors make informed decisions on whether to invest. A security’s unlevered beta also measures that security’s volatility and performance in relation to the overall market, but it takes out the effects of a company’s debt factors. Since a security’s unlevered beta is naturally lower than its levered beta due to its debt, its unlevered beta is more accurate in measuring its volatility and performance in relation to the overall market.

- By placing debt on a property, the amount of equity required is lower, which means that the investor earn a higher return on the amount of money that they put in.

- We defined these terms using single year capitalization rates, and also using multi-year yield rates.

- Working capital, or net working capital , is a measure of a company’s liquidity, operational efficiency, and short-term financial health.

- It’s typical to assess the value of a real estate portfolio on a quarterly basis to ensure the cap rate is still accurate.

A successful strategic transformation of the company formed the biggest source of management contributions to IRR. IRR Levered is calculated based on the levered free cash flows (another variation of this is to use a cash-in / cash-out consideration based on the initial equity investment made, dividends and exit proceeds). IRR levered includes the operating risk as well as financial risk .

In most of the US, however, returns like that are unacceptable to most investors. This is because investors are willing to trade some of this return for a highly liquid market like New York City. Even with the same annual cash flow and rent increases, the IRR is only 10% in this all-cash situation. While that is still a good IRR, it doesn’t come close to that of a levered deal. Levered IRR is the same calculation, except it takes a property’s debt into account.